Chapter 32 — Efficiency and Market Failure

Cambridge International AS & A Level Economics (9708) · Unit 7.3 · 4th edition coursebook

Learning objectives

- Define the meaning of productive efficiency and allocative efficiency.

- Explain the conditions needed for productive efficiency and allocative efficiency.

- Explain Pareto optimality.

- Define the meaning of dynamic efficiency.

- Define the meaning of market failure.

- Explain the reasons for market failure.

Key terms

- economic efficiency

- Where scarce resources are used in the most efficient way to produce maximum output.

- productive efficiency

- When a firm is producing at the lowest possible cost.

- allocative efficiency

- Where price is equal to marginal cost; firms are producing those goods and services most wanted by consumers.

- marginal cost

- The addition to total cost when making one extra unit of output.

- Pareto optimality

- Where it is impossible to make someone better off without making someone else worse off.

- dynamic efficiency

- When resources are allocated efficiently over time.

32.1Introduction to efficiency

The concept of economic efficiency stems directly from the fundamental economic problem. Efficiency is said to exist when scarce resources are being used in the 'best' possible way — that is, when the greatest possible level of infinite human wants is being met with those scarce resources. In agriculture, this means obtaining the maximum crop yield from a given area of land; in manufacturing, it means producing as much output as possible from a given set of inputs. Efficiency is a very important concept in economics: it is always judged to be desirable because it represents the best possible solution to the fundamental economic problem.

Economic efficiency consists of two components:

- Productive efficiency occurs when firms produce at the lowest possible cost. A firm is productively efficient when it is making the best use of resources and producing at the lowest cost possible — for example, a car assembly plant using the latest technology to minimise the cost of each vehicle produced.

- Allocative efficiency occurs when firms produce the combination of goods and services that consumers most want. Allocative efficiency gives consumers maximum satisfaction at their current level of income. The implication is that there is no waste, and that both producers and consumers are satisfied with what is produced. The price consumers are willing to pay reflects their preferences and the benefits they derive from consumption; it represents the additional benefit derived from the consumption of one more unit. Marginal cost — the cost of producing one more unit of a good — is a measure of the opportunity cost of the resources used to produce this last unit. So where price equals marginal cost, consumers are prepared to pay exactly what it costs to produce the last unit. It is only where this occurs that resources are efficiently allocated.

When both productive and allocative efficiency coexist, the best possible use is being made of scarce resources. There is efficient resource allocation.

Efficiency operates at both a microeconomic and a macroeconomic level. At the global level, economic efficiency is achieved when economies are using all of the world's resources in the best possible way; the use of protectionist trade policies demonstrates that global efficiency is often not being achieved. Several examples illustrate why efficiency matters across scales:

- Oil. The global supply of oil will eventually run out, yet consumption continues to rise in high-income economies and increasingly in lower middle-income countries and emerging economies. Growing populations, rising living standards and higher car ownership all push demand upwards. The use of oil is invariably inefficient: fuel is wasted through traffic congestion, the popularity of vehicles with high fuel consumption, and the inefficient use of oil and oil products in manufacturing. Achieving net zero climate targets requires far more efficient use of fuel.

- Timber. Global demand for timber and timber products such as paper and cardboard shows little sign of slowing. Much of the world's forest cover has already been destroyed, and the costs of this destruction are largely overlooked by the powerful global firms that control the sale of timber and pulp on world markets.

- Water. As the global population grows and the effects of climate change intensify, water becomes scarcer and an increasingly political issue. Tensions over shared natural water resources have already emerged between countries that draw on the same rivers. High-income countries often pay little attention to how more efficient use can be made of this essential resource.

- Trade. Trade agreements signed in line with the law of comparative advantage are intended to lead to greater efficiency in production and consumption — allowing countries to consume beyond their own production possibility curves. Agreements between trading blocs and middle-income economies are especially significant at a time of growing protectionist trends in the global economy.

Key concept link — Equilibrium and disequilibrium / Scarcity and choice

The need for economic efficiency is underpinned by the fundamental economic problem. It is essential that scarce resources are used in the most efficient way in order to maximise the benefits for producers and consumers.

32.2Conditions needed for productive efficiency

Productive efficiency exists when a firm produces at the lowest point on its average cost curve. At any higher level of average cost the firm could produce the same output more cheaply by reorganising the use of resources; at any lower level of average cost the firm is not using the available resources fully. Only at the minimum point on the average cost curve is the firm extracting the maximum output from each unit of input (see Figures 32.3 and 32.4).

Productive efficiency can also be illustrated using the production possibility curve (PPC). The PPC shows the maximum combinations of two goods that an economy can produce given its resources. Any point inside the curve is productively inefficient: more of both goods could be produced with the resources available. Any point on the curve is productively efficient because all resources are fully and efficiently employed. Points beyond the curve are unattainable with current resources.

Competition and productive efficiency

Competitive markets tend to push firms towards productive efficiency. Firms have a profit incentive to produce at the lowest possible cost — the lower their costs, the greater their potential profit. Failing to minimise costs in a competitive market may lead to bankruptcy because rivals will set lower prices and capture the firm's customers. In long-run equilibrium in a competitive market, firms produce at the lowest point on their average cost curve, which is the productively efficient level of output.

32.3Conditions needed for allocative efficiency

Allocative efficiency exists when the price of a product is equal to its marginal cost of production — the cost of producing one more unit of output. In this situation, the price paid by the consumer represents the true economic cost of producing this last unit of the product, and this ensures that precisely the right amount of the product is being produced. The value the consumer places on the next unit (revealed by the price they are willing to pay) is exactly equal to the opportunity cost of the resources used to make it.

The idea can be shown through a simple worked example. Suppose price is constant at $5 per unit, while marginal cost rises with output — $2 for the first unit, $3 for the second, $4 for the third, $5 for the fourth, $6 for the fifth, $7 for the sixth and $8 for the seventh. Producing only one, two or three units would not be allocatively efficient: the marginal cost is below the price the consumer is willing to pay, so the product is worth producing further — there is scope for further worthwhile production. Producing five, six or seven units would also be inefficient: at the seventh unit, for example, the marginal cost of $8 exceeds the $5 the consumer values it at, so resources are being wasted. There is one ideal output level — four units — where price equals marginal cost and allocative efficiency is achieved.

Unlike productive efficiency, allocative efficiency cannot be shown on the production possibility curve. Any point on the PPC could potentially be the allocatively efficient point provided price equals marginal cost at that point; the exact location depends on consumer preferences, which are not part of the PPC model.

A competitive market can lead to allocative efficiency. In such a market, firms are constrained to produce those products that consumers most desire relative to their cost of production. There are two motivations for this, mirroring the case for productive efficiency. First, the desire to make the greatest possible profit pushes firms to produce the goods consumers most want, because doing so leads to the highest possible demand and the greatest revenue and profit. Second, firms in competitive markets will be forced to produce those products most demanded by consumers — if they do not, other firms will step in and do so, and failure to satisfy consumer preferences will force some firms to close. In long-run competitive equilibrium, output is reached where price equals marginal cost — the requirement for allocative efficiency.

Allocative efficiency requires price to equal marginal cost. If MC is below price, the value consumers place on extra units exceeds the cost of producing them, so output should be expanded. Expanding output increases supply and so reduces the market price - hence production increases and price decreases is the change that restores allocative efficiency.

32.4Pareto optimality

Pareto optimality occurs when it is impossible to make any one person better off without making at least one other person worse off. It represents the best possible allocation of resources in the circumstances.

Pareto optimality can be illustrated on a production possibility curve. When the economy is producing at a point on its PPC, more of one good can only be obtained by giving up some of another — this is a Pareto-efficient allocation. At any point inside the PPC, however, it is possible to produce more of one good without reducing production of the other, so someone can be made better off without anyone being made worse off. Such points are Pareto inefficient.

When the existing allocation is not Pareto efficient there is scope for Pareto improvement: a reallocation of resources that makes at least one person better off without harming anyone else. In practice, most real reallocations create some winners and some losers, so genuine Pareto improvements are rare. Compensation arrangements may be needed if those made worse off are to accept the change. An airport expansion illustrates the difficulty: passengers and airlines gain from improved facilities, residents lose homes or are exposed to additional noise and air pollution. The case for the expansion rests on the overall efficiency gain rather than on a strict Pareto improvement.

A reallocation that makes someone better off without making any other person worse off is a Pareto improvement, and the process continues until no such reallocation is possible. So a reallocation of resources that can make someone better off without making any other person worse off is consistent with a movement towards Pareto optimality.

Pareto efficiency is reached when it is impossible to make any individual better off without making someone else worse off. The other options either describe inefficiency (output can rise with the same inputs, or reallocation can raise satisfaction) or relate to spare capacity. The defining condition is that some people cannot become better off without others becoming worse off.

32.5Dynamic efficiency

Dynamic efficiency is a long-run form of productive efficiency that benefits a firm over time. It is achieved when a firm reallocates its resources in such a way that output increases more than proportionally to the increase in inputs, often by introducing new production processes in response to competitive pressures. Where dynamic efficiency is present the firm's long-run average cost curve shifts downwards (see Figure 32.6).

Achieving dynamic efficiency requires investment, which may be financed from within the firm (for example out of supernormal profits) or from outside. The investment can raise costs initially, but the payback comes later in the form of lower long-run average costs. Firms that fail to invest in new processes and products risk falling behind their rivals and being forced to leave the market. The motor vehicle industry is a familiar example: innovation and large-scale investment in computer-aided design and automated assembly have raised efficiency and lowered production costs per vehicle over many decades.

Key concept link — Equilibrium and disequilibrium / Time

Efficiency and inefficiency can be explained in various ways. Efficiency and inefficiency are dynamic concepts: over time, markets and economies can move from being efficient to being inefficient and back to being efficient.

Dynamic efficiency describes improvements over time in the firm's ability to produce, lowering the long-run average cost curve through investment, innovation and learning. A fall in average total cost over time is the defining manifestation, so the form of efficiency illustrated is dynamic efficiency.

32.6Market failure

Markets do not always allocate resources efficiently. Market failure exists whenever a free market, left to itself with no government intervention, fails to make the best use of scarce resources. In other words, the interaction of supply and demand does not lead to productive and/or allocative efficiency.

The consequences and causes of market failure that the syllabus identifies include the following. Several are explored in more detail in later chapters.

- externalities in the market;

- the provision of merit and demerit goods;

- the provision of public and quasi-public goods;

- information failure;

- adverse selection or moral hazard;

- abuse of monopoly power in the market.

Whatever the specific cause, the underlying problem in each case is the same: resources are not allocated efficiently. When writing about market failure, students should always link the analysis back to this central idea. Market failure usually requires some form of government regulation or intervention to correct it.

Key concept link — Efficiency and inefficiency

Market failure arises because the free market mechanism is not always efficient in the way in which resources are allocated. As will be seen later, market failure invariably requires various types of government regulation to make good market failure.

Market failure is any situation where the free market fails to deliver an efficient allocation. Imperfect information, monopoly power and non-excludability (which causes public-good free-riding) all cause inefficient allocation. Income inequality is about how output is distributed, not about whether the allocation is efficient, so it is not a source of market failure.

End-of-chapter practice

Past-paper questions from CIE 9708. Pick A, B, C or D. Answers are saved on this device — press Download report (PDF) at the top to save them.

Market failure means the price mechanism does not deliver allocative efficiency. Atmospheric pollution from car emissions is a classic negative externality - drivers do not pay the full social cost of their journeys, so cars are over-consumed. The other options describe distributional or affordability issues, not failures of allocation.

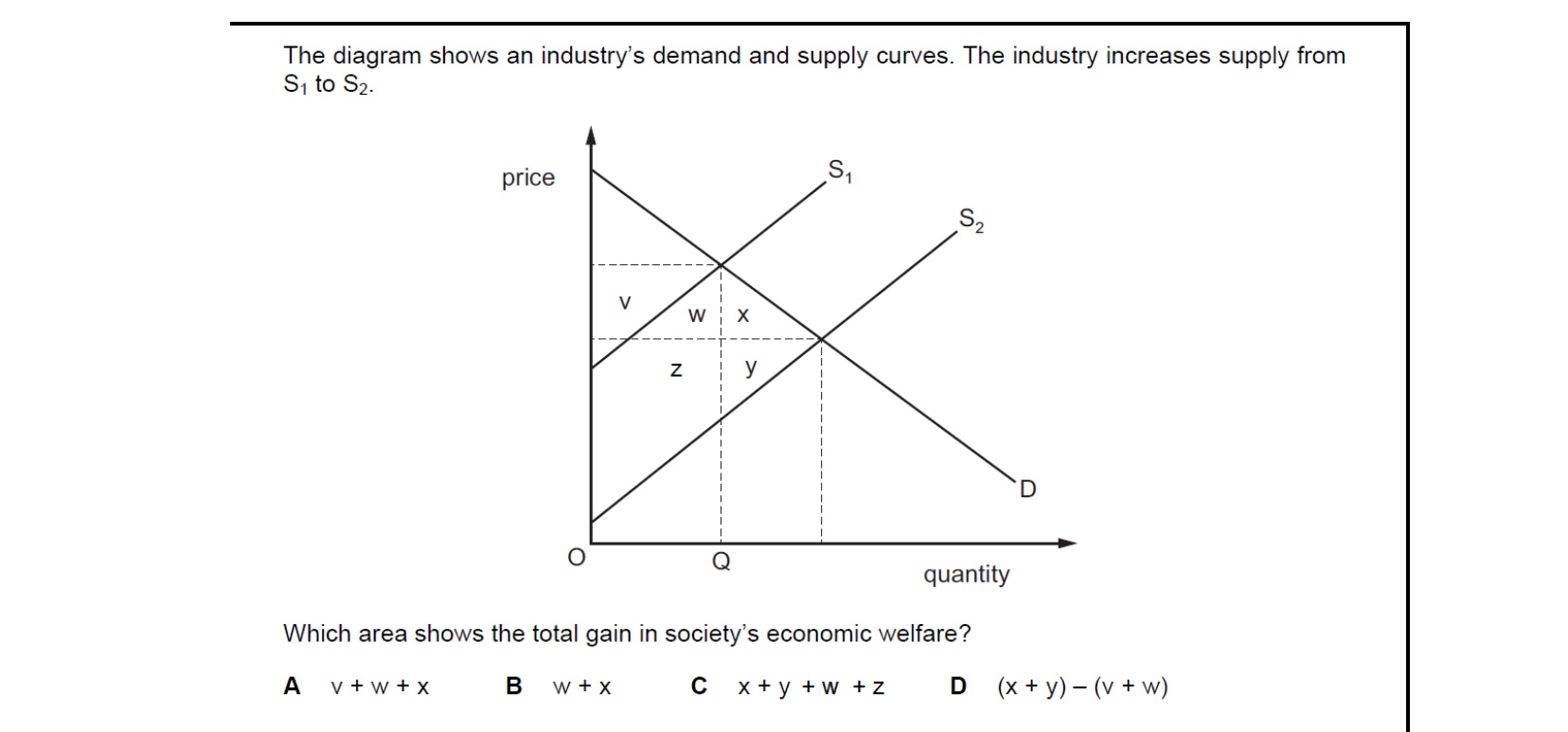

A free-market price rise in essential imported raw materials raises firms' costs and worsens the trade balance, but the relevant micro question here is welfare. With a supply shift from S1 to S2 the change in total welfare equals the new consumer plus producer surplus minus the old, which the diagram measures as area x + y + w + z - so the correct welfare gain is x + y + w + z.

Economic (allocative) efficiency requires that the marginal social benefit of producing one more unit of any good equals the marginal social cost. If MSB exceeds MSC, more should be produced; if MSC exceeds MSB, less. Efficiency is achieved only where marginal social cost equals marginal social benefit in the production of all goods.

Productive efficiency requires production at minimum average cost. Allocative efficiency requires price equal to marginal cost across all goods. The pollution example is a textbook negative externality - drivers do not pay for the harm emissions impose on others - making atmospheric pollution from cars in cities a clear example of market failure.

Productive efficiency means producing a given output at the lowest possible cost - that is, on the lowest point of the average cost curve. It is independent of externalities and of how price relates to marginal cost. The necessary condition is the production of a good at minimum average cost for a given output.

Attempt the practice questions above to build your score.

Self-evaluation checklist

After studying this chapter, you should be able to:

- Understand that economic efficiency consists of productive efficiency where a firm is producing at the lowest possible cost and allocative efficiency where price is equal to its marginal cost of production.

- Explain the conditions needed for productive efficiency and allocative efficiency.

- Understand how productive efficiency and allocative efficiency can be applied using a production possibility curve (PPC).

- Explain that Pareto optimality occurs when it is impossible to make an individual better off without making another individual worse off.

- Explain that the long-run concept of dynamic efficiency is a form of productive efficiency that benefits a firm over time.

- Understand that markets sometimes fail to deliver the most efficient allocation of resources.

- Analyse the causes of market failure.

- Evaluate the consequences of market failure.

Want more practice? Drill this chapter's past-paper MCQs (61 questions) →